A Better Way to Measure Consolidation Across Auto Services

Consolidation is one of the most frequently discussed themes in automotive services, but it is rarely measured with enough precision to be genuinely useful. Broad site counts and generalized market statistics often make for easy conversation, yet they can produce misleading conclusions when they combine business models with very different economics, capital intensity, and relevance to institutional capital.

That problem matters because a weak denominator produces a weak conclusion. A self-service car wash generating modest annual revenue has very little in common with a high-volume express tunnel that fits the profile of a scalable acquisition target, yet both are often included in the same headline industry total. The same issue appears across fuel retail, tire, and dealerships when raw industry counts are used without regard for operating quality, format, or scale.

This analysis takes a narrower and more useful view. Rather than treating every site as equally relevant, it focuses on the higher-volume, institutionally investable portion of four verticals: express exterior carwashes, qualifying gas and convenience stores, franchised new-vehicle dealerships, and higher-volume tire retailers. From there, it compares those cohorts using two familiar measures of concentration: the five-firm Concentration Ratio and the Herfindahl-Hirschman Index, or HHI.

The result is a cleaner picture of where consolidation actually stands. It shows not only which verticals appear more concentrated today, but also which still have meaningful runway, which are governed by structural constraints, and where the market narrative has become too simplistic.

Why most consolidation talk falls short

Much of the casual discussion around consolidation suffers from a basic flaw: it relies on top-line industry figures that are technically true but analytically unhelpful. When operators, investors, or advisers talk about total site count, total market size, or multi-unit ownership without first narrowing the population, they risk describing a market that does not really exist for the purpose at hand.

Carwashes provide the clearest illustration. It is common to hear there are roughly 60,000 to 65,000 carwash sites in the United States, but that figure lumps together radically different formats, including self-service sites and high-volume express exterior tunnels. Once the lens is narrowed to express exterior conveyorized tunnels washing more than 100,000 cars per year, the picture changes substantially, with a much smaller and more consolidated population emerging.

That same logic applies across the other verticals in this study. The relevant question is not how many total locations exist in some broad category, but how many qualifying locations exist in the part of the market that actually attracts capital, supports scalable infrastructure, and reflects meaningful competitive positioning.

A more useful method

To create a more decision-useful comparison, the analysis applies a deliberately narrow population screen to each vertical. Carwashes are limited to express exterior conveyorized tunnel washes doing more than 100,000 cars annually. Gas and convenience stores are limited to sites combining fuel and c-store operations at roughly 125,000 gallons per month. Dealerships are limited to franchised new-vehicle branded stores in the United States. Tire retail is limited to stores producing at least $1.5 million of annual revenue and offering tire and only basic maintenance services.

These filters matter because they align the denominator with the part of the market where most revenue, outside capital, and strategic consolidation activity are concentrated. They also likely overstate rather than understate the current level of consolidation, since institutional capital tends to concentrate first on higher-performing subcohorts. In that sense, the methodology is conservative in the opposite direction of most industry commentary: it does not manufacture runway by padding the market with irrelevant operators.

Two tools are then used to compare concentration. The first is the five-firm Concentration Ratio, which measures the percentage of market share held by the five largest players. The second is HHI, which measures how concentrated the market is across all participants on a scale from zero to 10,000, where 10,000 represents a pure monopoly. Each metric has limitations, but together they provide a much more grounded view than anecdotal commentary alone.

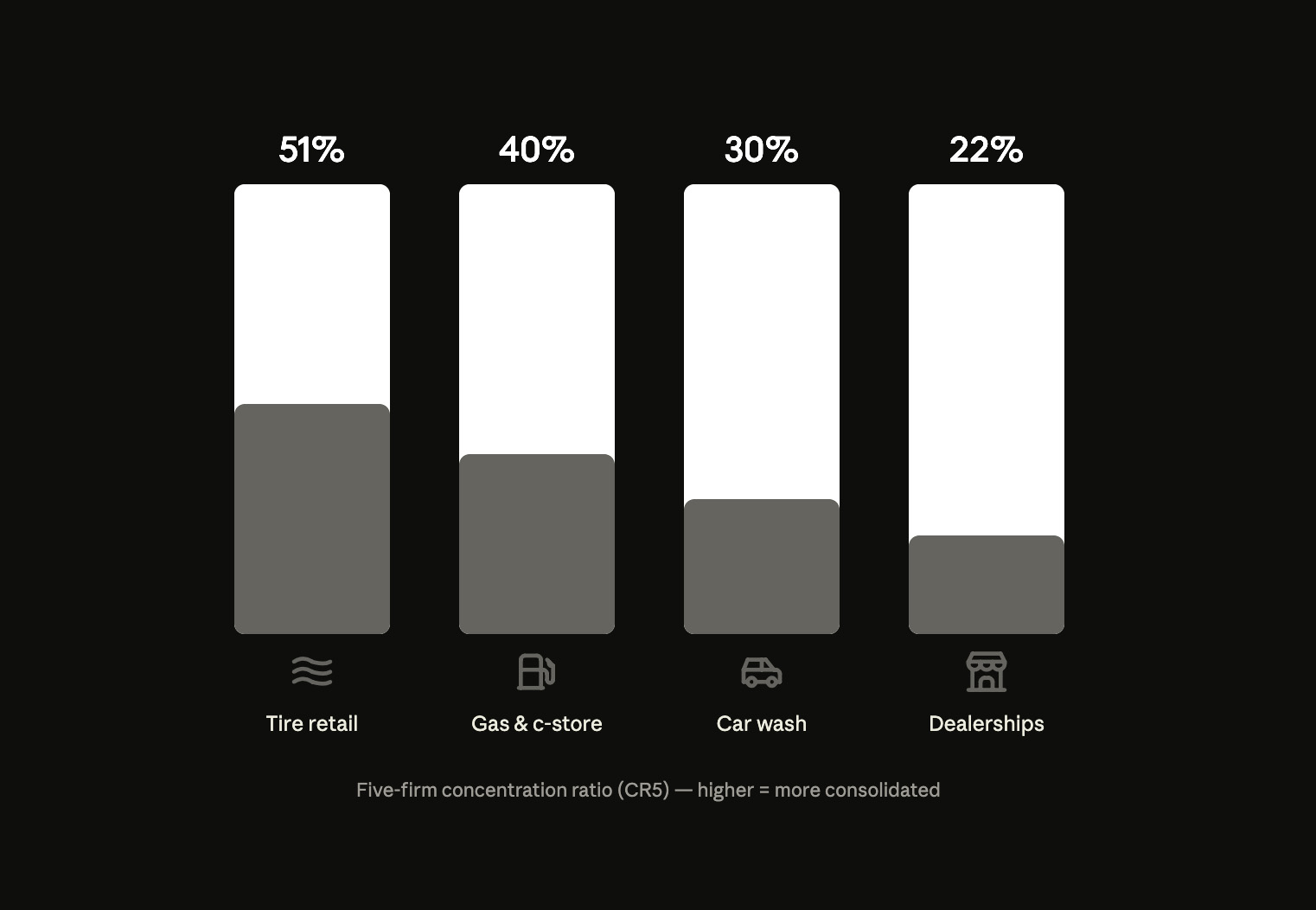

What stands out immediately

At a high level, the first takeaway is that none of the four verticals appears highly consolidated on either measure. Even the most concentrated of the group does not suggest a market that is effectively finished from a roll-up standpoint. That alone runs against the instinct many market participants have when looking at mature, visible categories such as gas stations or dealerships.

The second takeaway is that dealerships and carwashes appear less concentrated than tire and c-store gas on both the Concentration Ratio and HHI frameworks. That is notable because the intuitive ranking many outsiders might expect would place dealerships and c-store gas much further along the consolidation curve than the data suggests.

The third and most striking takeaway is that franchised dealerships screen as the least consolidated of the four. The draft analysis places the five-firm Concentration Ratio at roughly 22 percent and HHI at approximately 130, which is a surprisingly low result for a large, capital-intensive, highly visible industry. More importantly, that low concentration is not being created by a denominator packed with weak or trivial operators. The franchised model already filters for seriousness through capital requirements, facility standards, and manufacturer approvals.

Convenience stores and gas

C-store gas is, in some ways, the most deceptive of the four verticals. It has been consolidating for decades, beginning in earnest in the 1980s following deregulation in oil and gas and continuing through the divestiture of downstream retail operations by major oil companies in the early 2000s. Add private equity participation, procurement leverage, multi-site overhead savings, and the ability to support structured commodity hedging, and it would be easy to assume the sector must be close to fully rolled up.

Yet the measured picture is more nuanced. Despite its long history of consolidation, c-store gas does not appear fully consolidated by either the five-firm concentration lens or HHI. The reason is straightforward: the strategic logic for scale in this vertical remains strong. Procurement advantages are meaningful, overhead can be spread across a large network, and larger operators are better positioned to manage margin volatility and purchasing complexity than smaller independents.

That makes c-store gas one of the strongest examples of an industry where consolidation has been persistent for decades without being complete. The implication is not that the market has failed to consolidate, but that the underlying economics continue to reward incremental scale.

Dealerships

Dealerships are the most counterintuitive case in the set. By the measures used here, franchised dealerships are the least consolidated of the four verticals, with a five-firm concentration ratio of roughly 22 percent and an HHI of about 130. For an industry with this much age, visibility, and capital intensity, that is a surprising result.

What makes the result more important is that it is not an artifact of market noise. Unlike other automotive services categories, franchised dealerships are not heavily diluted by a long tail of marginal operators that materially distort the denominator. The franchise model itself screens out many subscale or unserious players, which means the low concentration reading is being measured against an already qualified population.

The strategic logic for dealership consolidation is real. Multi-brand ownership helps absorb swings in manufacturer product cycles and supply dynamics. Centralized accounting, compliance, marketing, HR, and CRM functions create overhead leverage. Larger groups can also secure more favorable floorplan financing and benefit from stronger used-vehicle sourcing dynamics, where scale itself attracts inventory and future acquisition opportunities.

At the same time, dealerships also face the most binding structural brakes. Ownership transfers are subject to OEM approval, franchise laws add friction, and manufacturers often impose formal or informal limits on how many points a single group may control. On top of that, the available synergies appear to flatten at roughly $1 billion in annual sales, after which additional scale adds more complexity than internal operating benefit. In other words, the runway is real, but it is governed.

Tire retail

Tire retail presents a different pattern: meaningful consolidation at the top, paired with persistent fragmentation at the bottom. The draft places the five-firm Concentration Ratio at roughly 51 percent and HHI near 704, which makes tire meaningfully more concentrated than dealerships or carwashes on headline measures. Much of that story is a private-equity story. The category offers predictable replacement demand, recession resistance, and clear procurement synergies, all of which fit the platform-and-bolt-on acquisition model extremely well.

The attraction is easy to understand. Tires are consumable and non-discretionary. Consumers may defer replacement briefly in a weaker economy, but they cannot do so indefinitely. That creates an unusual level of forecasting visibility for operators and investors, especially relative to more cyclical or discretionary retail categories.

Still, tire does not appear destined for complete concentration. The cost and complexity of starting a tire and basic-service shop are modest compared with other verticals, which allows new independents to keep entering the market. The local nature of trust and service also matters, as customers often return to the location or operator they know rather than to a national banner. Finally, buying groups and large distributors help independents access purchasing terms that partially narrow the scale advantage of larger platforms. As a result, tire looks like a vertical that can remain consolidated at the top while continuously regenerating an independent tail underneath.

Carwashes

Carwashes remain one of the clearest examples of why population definition matters. At the broadest industry level, the category can appear extremely fragmented simply because so many fundamentally different formats are counted together. Once the population is narrowed to high-volume express exterior tunnel washes, the relevant competitive landscape becomes much smaller, more investable, and more meaningfully shaped by multi-site ownership.

That narrower lens produces a very different strategic conclusion. In the qualified express segment, the market is far further along the consolidation curve than the raw 60,000-plus-site narrative would imply, yet it still appears to have room left to consolidate. This makes carwashes a useful reminder that the same industry can look either wide open or much more mature depending on whether the denominator reflects operational reality.

What this really means

The broad lesson is that consolidation should not be discussed as though every vertical is moving toward the same endpoint. Industries differ in the degree to which scale creates procurement leverage, spreads overhead, improves asset utilization, or drives sourcing advantages. They also differ in the forces that slow consolidation, whether those are regulation, franchise control, low barriers to entry, or the erosion of nimbleness beyond a certain size.

That is why applying one generic view of fragmentation across automotive services produces weak analysis. Some verticals, such as c-store gas, may continue consolidating because the economics of size remain compelling even late in the cycle. Others, such as dealerships, may have real runway but still settle into a structurally capped equilibrium because the market will not permit unlimited concentration. Others still, such as tire, may continue to show a split structure in which scaled leaders coexist with a self-renewing base of independents.

Seen this way, the central question is not whether consolidation is happening. It plainly is. The more useful question is where each vertical sits on its own path, how much economically meaningful runway remains, and what structural forces will determine its eventual resting point. That is where the analysis becomes practical for operators, investors, and advisers alike.

Advisory Services

Caruso & Co. advises owners, management teams, and investors across the automotive retail and services sector on mergers and acquisitions, capital raises, and strategic alternatives.

For confidential discussions regarding strategic or financial advisory matters, please contact Caruso & Co.